The International Monetary Fund (IMF) released its April 2025 World Economic Outlook (WEO): A Critical Juncture amid Policy Shifts, soon after the US announced its latest round of tariffs—to be implemented nearly universally. The US began instituting new tariffs in February, and, although some trading partners responded with countermeasures, market responses were not particularly notable. However, with the April 2 announcement, tariff rates rose to the highest levels in about a century—a negative growth shock. Major equity indices experienced historic drops followed by a partial recovery after April 9, when a pause and some adjustments were announced. The unpredictable nature of these tariffs has had a negative impact on economic activity, and uncertainty, especially regarding trade policy, has soared.

Throughout 2024, the global economy showed signs of stabilizing following the disruption of the COVID-19 pandemic and record inflation. Inflation rates were approaching target levels, labor markets returned to prepandemic levels, and GDP growth was in the 3.0% range. However, in the last quarter of 2024 and early in 2025, economic momentum waned, with deceleration of retail sales, investor sentiment becoming more pessimistic, hiring slowing in many countries, and inflation even rising in some countries,

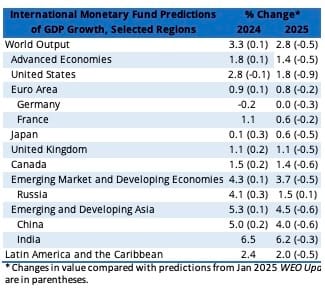

For the April WEO, given the uncertainty at the time of writing, the IMF based what it calls a “reference forecast” on the information available as of April 4 (including tariffs and responses). In this reference forecast, GDP predictions for 2025 have dropped 0.5 percentage point from the forecast from January’s Update for a gain of 2.8%. For most economies, 2025 GDP growth is expected to slow, with projections falling from those anticipated in January. These downward revisions are notable for Canada, Japan, the UK, and the US. Although the reasons for the slowed growth vary somewhat by economy, the uncertainty of tariffs and trade policy are a common factor. Major changes to Germany’s fiscal rule, and, in Japan, above-inflation wage growth resulting in stronger private consumption, are expected to increase the countries’ GDP growth in 2025. Another exception to declining growth for 2025 is the Middle East and Central Asia, where ongoing conflict is expected to lessen, as are disruptions of trade and oil production.

In the April WEO, global headline inflation is projected to drop to 4.3% in 2025, slightly higher than predicted in January. Global trade growth is expected to slow to 1.7%, in light of restrictions resulting from increased tariffs. The IMF predicts the increasing likelihood of further adverse risks, including an escalating trade war, social unrest (given the cost-of-living crisis and lowered medium-term growth prospects), and the intensification of international conflicts. On the other hand, factors such as new trade agreements, the mitigation of ongoing geopolitical conflicts, structural reform, and AI-fueled growth could cause more favorable outcomes.

Prospects for the analytical instruments industry are also less than favorable. In addition to challenges posed by uncertain trade policies and tariffs, major cuts to research funding and federal employees by the US government threaten to shut down research programs. Further, the administration’s antagonistic stance toward many elite universities, including deportations and restrictions on student visas, may decrease enrollment and research funding. All of these factors are likely to contribute to a decline in demand for lab instruments and other products.